In the long run, there are no point solutions in Vertical SaaS; there are only platforms. Small business owners want a single point of accountability, and while you might partner with other vertical SaaS vendors (VSVs) in the short term, don’t fool yourself—you will ultimately be competing over account control and downstream expansion cross-sells over time.

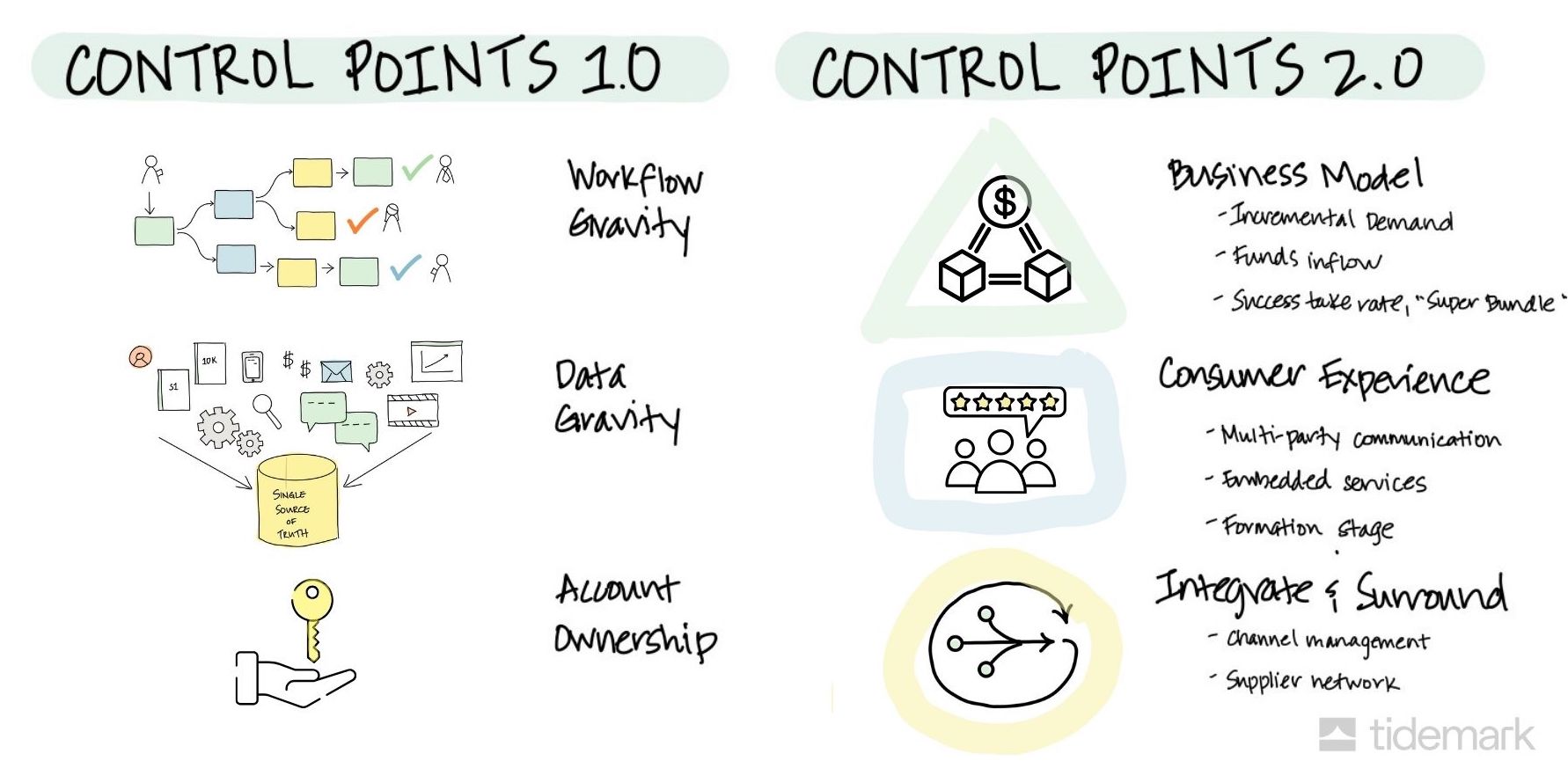

In Vertical SaaS, there are typically one or two control points, or systems of record.On a fundamental level, the control point is the most important system, the last to be thrown out before an owner ceases operations. One of these is in the front office (i.e., point-of-sale, CRM, or e-commerce). This control point drives sales and serves as the cash register. The front office control point is accompanied by one in the back office, home of the general ledger to which everything is reconciled. If you own a back office, the goal of a VSV is to build or acquire the front. Own the high ground, own the control point!

Control points have this power because of the three types of VSV gravity:

Winning the control point is not easy. By definition, a system of record is hard to displace. Unless the market is literally pen and paper, a VSV will be fighting highly entrenched software companies. You may be able to do it organically with product innovation, but M&A can also be an option if the integration debt is manageable. If M&A is not possible, a slow winnowing of your competitor may be the only approach available.

This winnowing can happen by having an even more in-depth understanding of control points beyond the three types of gravity.

As the Vertical SaaS industry has developed over the last few years, we've learned that other offerings can also serve as control points. These new control points can act as wedges to either capture the traditional control points, or subsume them entirely. They can either impact a merchant’s business model or improve the end-consumer experience.

In Vertical SaaS, bringing in customers beats most other value propositions. It is doubly powerful because a VSV bringing in demand allows the merchant to fund the purchase of the VSV’s other software products. In the extreme example, if a VSV can generate demand, it can charge a take rate on demand that allows it to offer disruptively low pricing on other products.

However, a VSV doesn’t need to provide demand directly. It can also generate incremental demand by increasing customer access through financing (buy now, pay later), conversion through customer confidence (certification, fraud, etc.), integration into more demand sources (e.g channel management), or new customers and repeat rate through CRM and loyalty programs.

Similar to revenues, a merchant can grow more quickly if a VSV can provide credit, insurance, or improved working capital management. However, credit can be a commodity, so it is rarely enough to bring in funds alone. To be an effective wedge, the provision of credit is usually accompanied by several conditions: